Investing is easy but not simple. Investing can be skinned in many different ways creating possibilities that are extremely far off from each other yet produce similar results over the long run. Emotional equanimity through the process is a completely different animal with varied outcomes depending on the part of the cycle one is in.

While markets are largely efficient, it is just as often extreme in its views of certain sectors of the market. Either investors are completely enamoured by the business and its quality that they want to own it at any price and project the future with a lot of certainty that the underlying business might or might not possess. On the other hand, they completely shun some businesses and refuse to touch it even when the value proposition gets compelling. Couple this phenomenon with the narration bias where glowing articles galore on businesses that do well and doomsday articles on businesses that rile on businesses that are out of favour. This creates an interesting pond of opportunity as the market analyses the information fairly well but there are times when the market also struggles to separate the wheat from the chaff. Other times, the narration changes very quickly.

Let us look at a business that is viewed very favourably today by the market. Apple Inc. The market cap of Apple is $1.395T today and the shares trade at $318.31 as we speak. The PE is north of 26 and the dividend yield is just shy of 1% (Yahoo Finance) The market is pricing in what is expected to be a strong holiday season sales; the subscription growth of Apple+, the newly launched streaming service last year; the AirPods pro launch and the upgraded iPhones; the 5G compatible phones that are expected to be released later this year. All are valid reasons and you can find several articles that dissect any of the above mentioned reasons and you can get a fairly good sense of the narrative. All in all, it is priced like a technology leader who relevancy is solid with a strong moat that will protect the business (at least for the next decade).

Rewind a year ago, the market cap of Apple was close to 50% of what it was today. Jan 21, 2019, Apple closed at $157.9 a share; a tad less than half of today’s price. In less than a year, the company has added close to $700B of market cap. Around the same time last year, the company was coming of a bad holiday season, profit warnings, gloom and doom articles appeared around how companies could bypass the App Store and even though Apple was better than RIM and Nokia, it faced an uncertain future in a technology driven market and was much better priced at a lower valuation like a declining business.

What a difference a year makes. In context of Apple though, it needs to be kept in mind that the market does not owe a down year just because it had a stronger than expected 2019. Nor does it mean that the momentum will continue forever either. Remember, the market is supposed to be largely efficient. Yet, the narrative changes quickly. This is why investing is simple but not easy. 8.2% of the entire S&P growth in 2019 came from Apple alone. Apple and Microsoft, accounted for 15% of the S&P growth. If you owned the market, you benefited largely from the technology growth of 2019 or if you owned Berkshire, the value of your holdings benefited from Apple (as the single largest equity held by Berkshire). If you were a single name investor and did not have the index or Apple or Microsoft in the portfolio or were not big into FAANG or technology in general, you had an uphill battle in 2019 to beat the market.

However, that was an easy one. If you are investing in the markets, you probably were aware of the Apple example. If you had to benefit from Apple’s massive run, you had to buy / hold the stock through some scary headlines. Just being contrarian does not work either. Every bankruptcy has been preceded with scary headlines. Differentiating the wheat from the chaff is the key there.

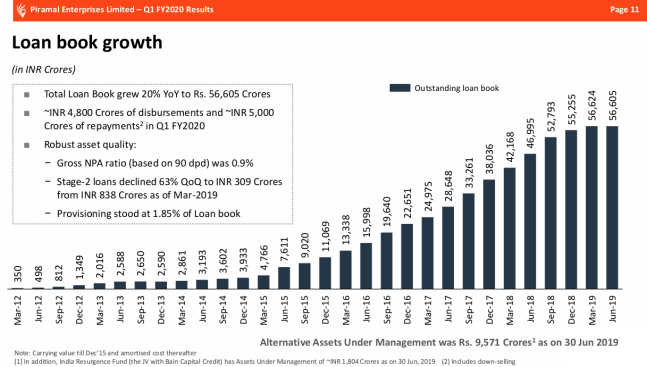

Let us look at some examples at the other end of the spectrum. Pan out from the US and pan in into the Indian banking and shadow banking system. A poster child of things gone wrong. DHFL posted close to a $900M loss on a $14B loan book; financial irregularities are being investigated and the company is going through a bankruptcy process in India. Yes Bank is losing all credibility in the market for waffling around instead of raising capital. As of 30th Sep, the bank had a book value of INR 109, the market clearly does not believe that Yes bank is still marked properly. It has valued the stock the close to 40% of the reported book value. Very rarely have banks that have fallen more than 90% recovered quickly from debacles like this. Even if one were to assume that the bank was technically insolvent because liabilities exceeds assets, there is still a large piece of the balance sheet that is healthy that will earn positive cash flow and earnings. The only way in the medium term, the bank can come out of the mess is through a cap raise. Then the question becomes. at what margin of safety will investors be willing to invest capital in the bank? 50%? 60%? 90%? If the bank is not able to raise any capital even at a massive discount to the book value, they might as well go the same way as DHFL. In the case of no capital being raised, the market essentially signalling that it has no trust in the bank and with no trust, there is no banking. If not, they need to quickly raise capital and reverse the downward spiral they have been on for the last 24 months.

Examples like DHFL and Yes Bank coupled with a beleaguered real estate sector, growing NPA’s and slowing growth in India has resulted in separating the perceived very good banks and non-banking financial companies (NBFC’s) in India from the rest. Companies like HDFC, HDFC Bank, Bajaj Finance that are perceived to have less risk continue to enjoy a massive premium over the rest of the sector. They trade at huge multiples of book value, enjoy strong growth, low NPA’s and solid ROE’s and capital cushion.

But the interesting companies are neither of these two buckets but the ones stuck in the middle. The in-between bucket today neither enjoys the premium of a strong franchise nor the discount of a capitally starved financial institution. They are associated enough with the mess that the valuations are discounted due to association effects but decently high enough due to their earning power and robust business models. A decent example of both would be Shriram Transport Finance and Shriram City Union Finance, both of which we have been following (and owned) for years. The stocks have gone nowhere over the last few years even though the capital position is robust, earnings are increasing, the valuations are decreasing. Shriram Transport, which caters to financing of used trucks and new trucks, is largely dependent on the small owners of commercial vehicles. While at first glance, the NPA’s or the stage 3 ECL’s look high; they are more a function of the business model than they are of the underlying business. With a low LTV and a solid guarantor system, the realized losses are far lower than what the NPA’s or the ECL’s suggest. With a ROA close to 2.5%, ROE of close to 17%, Book Value of INR 751 and decent growth of AUM and decreased corporate tax rates, the stock is expected to earn around INR 125 this year and is trading at INR 1050 as of today. The market seems to be projecting the gloom and doom of today well into the future. Shriram City Union Finance, which caters to the SME sector and the MSME sector, is a similar story. With ROA north of 3.5%, ROE north of 17%, low leverage, a segment that is almost captive, high ECL’s but low real losses on loans, with a book value of 1031 INR at the end of Sep is trading at INR 1380 creating interesting possibilities. However, if you owned one of these in the last few years, the stocks and the portfolio went nowhere. Coupled with some big investors and PE looking to cash out, near term tailwinds are capped.

In this context, if one were to tether oneself to beating the market index while picking individual names, one would have to gravitate towards the momentum driven stocks or high quality stocks which are at sky high valuations. On the other hand, if one were to look at through the cycle growth and compare them, the risk-reward function might be changing. So far, the momentum and high quality stocks are miles ahead in the race.

As I am thinking through these examples, there are three broad lessons that I think of: 1. It is very tough to predict markets short term. But through the cycle, they will reflect the fundamentals of the business. 2. Markets are largely efficient but far from always efficient as seen by the Apple example above 3. One can have different investing approaches — the more I think, the more I am inclined towards being more conservative through businesses that have earnings on hand today, trade at low multiples to cash flow than predicting longer term cycles.

Disclaimers: Own several indexes, Banks, NBFC’s, Single Name stocks etc. See FAQ’s. Not recommendations. Please do your own research.