The markets have been unforgiving in many different ways. Off late, the route the market has taken is to sell all risk and get into safer instruments. Entire sectors have been brushed with a broad stroke and left to bite the dust. One such sector is the NBFC sector. While opaque accounting, financial shenanigans and unconstrained lending in the name of growth has brought some well deserved nails on some coffins, there are others that have been dragged down by sheer association.

I believe that Shriram City Union Finance is one such case.

SCUF is a deposit taking NBFC that serves the predominantly in the south with a sizeable operations in the west of India as well. They serve the underbanked, specifically the self-salaried and MSME who get easier access to NBFC’s (shadow banking system) as compared to banks.

The security closed on March 27th at INR 765.35 / share on the NSE. The market cap is INR 5,332 crores with ~6.6 crores shares outstanding. The security has a book value of INR 1070 per share or INR 7,062 crores. First nine months earnings for 2019-20 were INR 128.38 per share or INR 845 crores. 2018-19 full year earnings were INR ~150 / share or 988 crores. AUM was 29K crores.

SCUF is earning around INR 43-44 per share per quarter and growing. The market is valuing the entire company at 4.5 times earnings or earnings yield of 22%. It will be worthwhile to take a look deeper into what might be driving the same. A quick snapshot of the financials is as seen below.

As you can see, the company has fairly good NIM, high spread, good ROA and ROE and fairly manageable leverage. Furthermore, CRAR seems to be good and decent cash on hand as well.

Since the company serves the self employed and small businesses, the GNPA and NNPA is higher than usual but the company has managed fairly well in the past on the actual write downs. SCUF has been conscious of the market it is serving and has managed with lower LTV ratios, stronger security, higher spreads and a good ecosystem to manage collections. The situation before Covid was as follows:

There are several factors that would have impacted the business or caused the valuations to drop.

- Covid impact and net payments

- Concerns on repayments

- Liquidity in the market

- AL mismatch and liquidity concerns

- Corporate governance

Covid Impact: It is very early to estimate the real impact of Covid. This could go several different ways but I think we can draw large enough boundaries and what the expected outcome could be for SCUF. Just because of the sheer segment that SCUF lends to, we should expect a lot of stress. The small businesses are on the first line that will get affected by Covid and the subsequent economical slowdown that comes along with it. There are broadly two lines of thoughts that investors are divided upon: one is that this will be a short disruption, everyone self isolates, the virus dies and we have a V-shaped recovery. The other narrative is that because of the exponential growth in the cases we have been having, it will be many quarters or years before it becomes business as usual again.

In the former case, there are two more tailwinds that are there: RBI has provided permission to defer payments for three months, interest will continue to accrue, and the effects of the virus will be short-lived. Even if we assume that the operating expenses of the company will not come down, it will cost the company INR 375 crores with no income to keep the shutters open and incur every single rupee to keep the shutter open. This will impact the business around INR 57 / share. One quarter of earnings lost. This is like losing a dividend check. With the NPA rule being waived, it is the best case scenario.

In the latter case, beyond the initial tailwind due to the deferral from RBI, if things deteriorate further, we could see customers falling behind on payments, GNPA and NNPA spiking up and write off spiking up as well. Given the P/B of 0.71 that is the market is attributing indicates that they expect this scenario to play out. The market is expecting a INR 1700 crore write off (as of today) from this episode or close to 6% of the entire book (net of assets recovered) as an outcome of this prolonged exposure in the market. The markets that provide us some advance information is the China and the South Korean market. Things are recovering back but at a slower pace. I think it is fair to assume at this point that the same may repeat in India as well. It will eventually recover but at a much slower pace than most people expect. A fair amount of this write-off is already baked into the price. Why will the write offs not be higher? We will address it in the repayments section.

Repayments:

Here we need to digress a bit to understand the culture of Shriram and why ultimate repayments are Shriram will be higher than what we would think in a conventional sense. Shriram group hires people from the same social standing and the communities as their customers. Since they were serving the underbanked, their offices are frugal as as possible and they speak the same layman language as that of the customer. Furthermore, they are connected to the customers at the place of business and are well versed with the balance sheets etc. The credit process is designed in a way that the branch manager, who is effectively connected to the community is responsible for the approvals and is also held very responsible for the collections as well. Typically, customers prefer to work with Shriram group in general because of two main reasons a. they had a connection with the branch manager and an existing relationship. The system and offices were designed in a way that it would not scare the customers and would make him feel like he was borrowing from someone just like himself. b. compared to a bank where they would have to wait for 45 days to get a loan sanctioned, with the right data, they could get a sanction within 48 hours at Shriram. Furthermore, most of the customers getting a loan from Shriram City already have a relationship with Shriram Transport or Chits or insurance or have an existing relationship with the branch with a manager. Coupled with the fact that most of the loans are with low LTV / higher security than required, incentives aligned with a branch manager who is responsible for collections and a connection to community, defaults are on the lower side than what one would expect from this clientele.

This ecosystem is not going to change anytime soon. While the clientele will be hit by Covid, it is fair to assume that the branch manager will work closely with the customers to figure out the best possible way to get repayments done. The last thing the branch manager or the customer wants is a security pulled in from someone in the community. This has been evidenced through low real losses through previous recessions. However, it must be clearly noted the repayments are different from reported NPA’s. It is safe to presume that GNPA’s and NPA’s / stage 2 and 3 assets will spike but ultimately will get repaid. The repayments will depend on the pace of recovery more than anything else.

Liquidity in the Market:

It is no secret that Piramal has been trying to pare his stake in Shriram for a while now to further boost capital at the Piramal group. There will be always be a hang over the stock that over 10% of the shares outstanding will trade. If Piramal decides to sell in the open market like they did with STFC, it will create a glut of liquidity pushing the prices further down. However, it does look highly unlikely something would happen at these prices. It is a good 33% lower than where Piramal took his stake and I just don’t see him selling at these prices. Furthermore, TPG is trying to exit SCUF parent company at Shriram City as well.

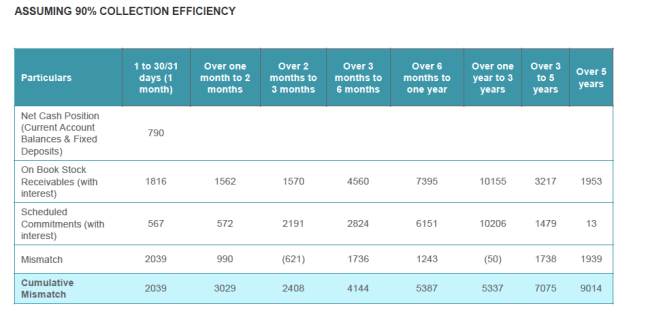

AL Mismatch and Liquidity concerns:

This will be a quick back of envelope calculation: If one assumes that Jan and Feb was business as usual at Shriram City, you will see that they would have excess liquidity of 5000 crores. This will need to be netted for disbursements that would have happened. If you use the prior quarter number, it is around INR 1900 crores per month. This would have left around 1200 crores in excess liquidity. Their cash balance was another 800 crores. Their scheduled repayments was ~2200 crores in March. With a collection efficiency of 10% in March, they could meet that. I am sure the number was a lot higher. Now with the NPA moratorium, I think it will provide some relief to Shriram repaying back its creditors as well. Over the 4 next months (which I think will be more like 6 months with the RBI moratorium), they will own around INR 5000 crores out of which they have access to 2000 crores; and receivables of INR 6,200 crores. If the collection efficiency is above 50%, their ALM will be fine over the next 6 months. However, one needs to account for the CET ratio and minimum cash they will need to maintain as per regulatory norms etc. If India does not get back to 50% of its efficiencies over the next 6 months, we are going to have much bigger problems. Given the current situation, I think they are sitting okay for now. Unless the situation deteriorates extremely badly, I think they will do okay. On top that, the conservative balance sheet will continue to have access to the capital markets. While the interest rates might wary, it is tough to imagine a balance sheet like Shriram city shut from capital markets.

Corporate Governance Concerns: I think between Shriram Capital, Transport Finance and City Union, the Shriram Group has shown a fair amount of good corporate governance till date. We have had RT leading the group, Ajay Piramal and there has not been a peep about governance. They have taken their lumps where needed and moved on. Nothing to indicate that minority holders are at an disadvantage at this point. We will need to see who will be at the helm once Piramal moves on.

All in all, while there are headwinds that SCUF is going to face, at ~22%+ earnings yield most of these concerns are baked in. Investors need margin of safety. The company is trading at 70% of liquidation value. They are yet to lose money in a single quarter. They have the ability and the cushion to lose money for a while and still be okay. The ecosystem is still firm and recovery will be on the back of companies like SCUF. It does provide an enterprising investor with a variety of possibilities.

I am interested in your thoughts and comments. please mail me: contact@beowulfcap.com

Disclosure: Long several NBFC’s and Banks including Piramal, SCUF, STFC.

Disclaimers: See FAQ here. Not a recommendation. Not a registered advisor. Just sharing my thoughts.