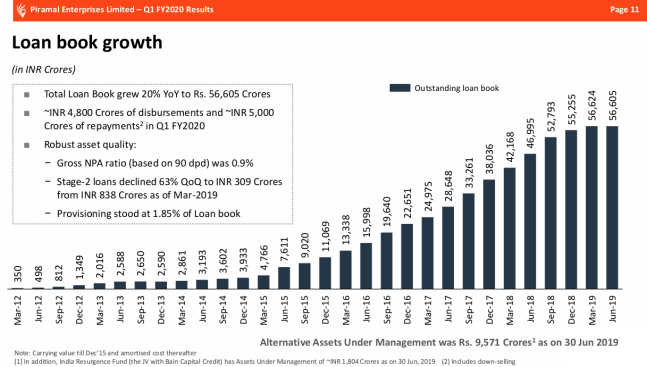

We had written about Piramal Enterprises before here recently. Last night, they announced their results. Strong revenue and profit growth at 21% YoY. As expected, the focus on was their financial services portion of the business. The book was flat quarter or quarter with about 5K crores of repayment and 4.8K crores of disbursements.

The real estate book is starting to show signs of diversification with a lower wholesale residential RE portion but it is still 47% of the book.

The ROA and ROE seems to be holding up well for the business. GNPA actually fell in the quarter based on 90 dpd. It does look like payments are coming in through for Piramal as of now. I suspect there is a lot of advance payments that is going on here that is causing this to look very strong and probably some better risk management as well.

A detailed book sensitivity shows that there are probably around 10% of the deals that need attention which is not concerning given that Piramal has shown an ability to actually implement corrective action and fix them in the last few quarters.

The key news was on the liability and equity side. The company informed that they were planning to bring in 8K-10k crores of equity on what they called significant growth and consolidation opportunities that are opening up on the NBFC.

I will also link here the CNBC transcript that shows a more aggressive yet cautious contrarian waiting for the right opportunities to open up in the NBFC space. It was good to see that they are treading with caution and watching instead of jumping into the first deal they get. With a solid quarter behind them, will this be a case of yet another counter cyclical aggression from Piramal? Only time will tell.

Disclosure: Long Piramal.