Piramal closed on March 20th at a market price of INR 684 with a market cap of INR 15.4K crores. The shares outstanding as of Dec 31st was 20.45 crores with a dividend yield of 4%. Given the fall from grace the stock price has experienced, it will be worthwhile to examine both the liability side and the asset side and summarise what we know.

Networth:

- Company capitalisation and access to capital: A classic example of this was Yes Bank where they struggled to raise capital and the bad loans soured and the RBI stepped in. However, that is not the case with Piramal. With the recent cap raise and the sale of DRG, the net worth is estimated to be close to 34K crores or INR 1382 / share.

- DRG: Clarivate has confirmed that is has closed the DRG for $950M with a payment of $900M to Piramal Enterprises which amounts to close to INR 6K crores. You can see the link of Clarivate’s SEC filing here on March 2nd. We can safely assume that this INR 6K crores is available to Piramal for now. This is approximately 39% of the market cap of the company as of March 21st.

- The rights issue for INR 5,400 crores that the company executed in Jan was fully subscribed and the company has received the proceeds. It is important to note that the promoters of the company fully participated in the rights issue. This is another 35% of the market cap of the company.

- Less than 9 months ago, the company sold its stake in STFC for 2,300 crores.

- It is clear that the company has had access to liquidity from the stake sales very close to the market cap of the company today.

- In addition, the company has announced the monetisation of the Shriram stake, which is estimated to bring 7-8K crores into the coffers. However, it needs to be seen whether with the economy further deteriorating drastically and the Covid impact whether the Sep timeframe given by the management holds good.

- Furthermore, the company has announced that they are considering a stake sale of 20% in the Pharma business and the proceeds here will fund the further growth of Pharma and will ensure that any incremental capital is available for the financial services business.

Liabilities:

- The company needs to have the ability to roll over the debt or repay the debt over the next few months to a year while the economy suffers from both a prolonged real estate crisis and the impact of Covid.

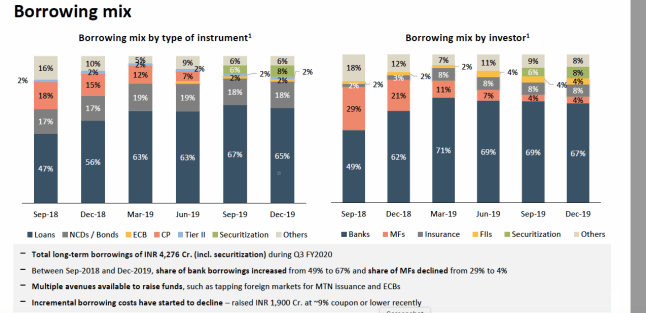

- The company has moved from reliance on commercial paper and reduced the exposure from 18K crores 18 months ago to negligible amount as of Dec 2019.

- It has gone into longer term bank debt and bank funding has increased from 49% to 67% of the total borrowings. (See appendix A for points 2. and 3.)

- Recently, the company has accessed 1,900 crores at 9% per annum which provides further comfort that the cost of funding is coming down.

- What is even more important in my opinion is that the banks have had access to the books and have examined closely the assets of the book before lending to Piramal. This was confirmed by the management during one of the recent conference calls on March 12th. (Appendix B)

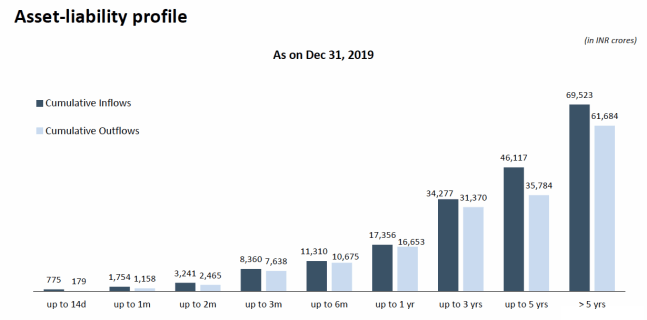

- The other thing that NBFC’s have to worry about is the ALM mis-match. Appendix 3 shows that close to 17K crores outflow is expected up to the next 12 months. Given the fact that they have close to 4.5K crores cash, Pharma generating proforma 1.5K crore operating cash flow over 12 months, capital raise and access to cash, high CAR of 32% before considering any payments coming from projects being refinanced or closed or the book run down, there should be a fair amount of comfort that the company will be fine in the next 12 months.

Asset Quality: The wholesale financing book is what seems to have scared the investors the most.

- The total finance loan book is INR ~51K crores. Housing finance is 6K crores, commercial real estate is 11K crores, CPG and ECL is 9K crores and the big chunk which is the residential real estate is 25K crores.

- So far, the company has reported only 1.8% GNPA and 1000 crores of provisioning so far. Again, given the recent experience with Yes Bank, the investors are being wary of companies that have exposure to stressed sectors but reporting very little GNPA and defaults.

- Firstly, it must be noted that, Piramal did not have any exposure to Yes Bank, Altico, IL&FS, DHFL, ADAG etc. which have gone bust. The fact that the company has dodged exposure to these stressed accounts indicate a certain level of quality of the book. Unlike Yes Bank, which had exposure to every stressed asset, Piramal seems to have dodged the bullet so far.

- In the housing finance segment, there is speculation that the government might provide some relief to MSME and non-salaried people towards EMI’s to help through the Covid situation. Hopefully, they will provide extended DPD guidelines to NBFC’s as well. Even if not, the GNPA’s might spike up. Unless Covid paralyses the economy over the next 6-12 months and things don’t get back to normal, the risk in the actual underlying defaults will be negligible. It must also be noted that the company has stressed multiple times that it is providing adequate LTV and security provisions in its loan book.

- The commercial real estate has not seen much stress in the last 2-3 years. Unless something new comes up as part of Covid and extended significant delays in construction, it would be fair to say that the commercial book will be fine.

- The corporate lending groups with its 9K crore book will see stress. We know that the Delhi Baroda truck financing with exposure of INR 75 crores is stressed. The Essel exposure from Piramal is close to INR 200 crores now. We should clearly expect to see more slippages from this and the GNPA shoot up over the next few months.

- The real estate wholesale financing segment is 25K crores. Piramal has run down close to 10K crores of the this segment over the last 18 months. The number of developers who were more than 15% of the net worth of the company has come down to 4 to 1. The one is Lodha.

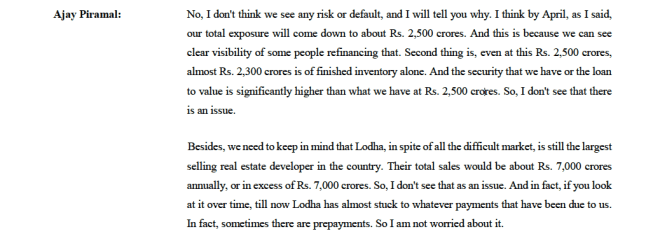

- Lodha will have a INR 2500 crore exposure to Piramal by April. A couple of positive developments. In the recent call, it was clarified that the capital under security for this loan is close to INR 6000 crores (Appendix D) Finished goods inventory is close to INR 2300 crores with another INR 1000 crores completing over the next 3 months. In addition, Lodha just tapped the capital markets to refinance and repay bonds. See link here. In addition, the last 12 months sales for Lodha was close to 7000 crores and continues to the largest real estate developer in India. While the current Covid shutdown and the resulting economic bumps might stagger payments, it is highly unlikely that Piramal will need to take a write down on Lodha.

- In addition, it is worth noting that some of the accounts that Piramal has in stage 3 assets, they are moving to get the title of the lands and recover the loan. Easier said than done but the company has demonstrated that they can execute such moves well in the past.

- So far, the company has demonstrated that is can manage the risk and the recoveries from customers that it is lending to, have a low LTV ratio and a better than average risk monitoring system.

- It must be noted that no way does this mean that the loan book won’t sour in the near future or the stage 2/3 provisions will need to go up and more money needs to be set aside for provisioning, all we get comfort from is that the fact the management seems to have demonstrated reasonably well that it can manage the risk it is taking on.

Management: Understated in the market is what I call the Say-Do ratio of the management. Lots of companies make promises but it is execution that matters. Contrast the equity raising by both Yes Bank and Piramal around the same timeframe and the results each of them has had.

- Raising of capital through rights sale

- Completing the promise of bring in 8-10K crore equity into the business

- Reducing reliance on commercial paper. The management laid out the roadmap 12 months ago.

- Reducing reliance on exposure to single borrower names

- Piramal has put balance sheet strength over sheer growth reversing the earlier stance.

- The only con that I can direct to the management is the fact that they did not build a Fort Knox balance sheet from the start and had to go through several stake sales, cap raises (albeit at a premium to today’s stock price) to build a solid balance sheet. However, the management has shown that it will learn and correct mistakes quickly.

Unless it comes to light that the management is completely fraudulent, it is reasonable to assume that Piramal will weather the storm.

Valuation:

- The December end shares outstanding was: 20.5 crores. With INR 5,400 crores coming in at INR 1,300; approx. 4.2 more shares would be added. The total new shareholding will be at 24.6-24.7 crore shares.

- Total net worth at INR 34K crores or 1,382 per share and CMP is at 684 or 0.5 P/B.

- Total borrowings are at 50K crores.

- Enterprise value is at 64K crores: 50K borrowings + 14K market cap.

- SOTP would be as follows (following Dec 2019):

- Shriram stake – INR 6-8K Crores

- DRG Cash – INR 6K Crores

- Rights issue – INR 5.4K Crores

- Commercial RE – INR 11 K Crores

- Housing Finance – INR 6K crores

- Pharma business – INR 15K Crores (@ 10X EV/EBITDA)

- Cash – INR 4.5K Crores.

- Sub-total of assets before residential RE and CPG/ECL assets is approx. INR 56K crores.

- The market is today valuing the INR 34K crores worth of assets at less than INR 10K Crores. It can also be reasonably shown that the INR 2.5K Crores to Lodha is reasonably safe. So, the market is valuing close to INR 31K crores of others at INR 7.5K crores.

- Depending on the risk appetite of the investor, it will open up interesting possibilities.

I am interested in your thoughts and comments. please mail me: contact@beowulfcap.com

Disclosure: Long several NBFC’s and Banks including Piramal.

Disclaimers: See FAQ here. Not a recommendation. Not a registered advisor. Just sharing my thoughts.

Appendix A:

Appendix B:

Appendix C:

Appendix D:

Just want to add one point. I think the Generally Accepted Accounting Principles and NPA classification of whole financial sector disguise the true picture the company. It doesn’t depict the true profitability. As compared to Yes Bank, i like the collateral of Piramal. The lend against the property rather than other instruments like equity shares, etc. The LTV ratio contains good Margin of Safety, which may deter the borrower from default intentionally. Just want to know if we can work out the real profitability of these NBFCs.

Disc. Invested

mailid: rughanikashyap@gmail.com (Further communication)

LikeLike

Agreed. I am also not biggest fan of the blackbox accounting of NBFC’s and Banks. Too many ways to evade the NPA rules. On the other hand, there is also too much of a broad brush is being used by the market to value some of these companies.

B. ________________________________

LikeLike

I am of the view that these NPA rules are too strict for the real estate sector especially. The normal term loan and real estate sector can’t be viewed with same glass. There has to be some relief for the same in this liquidity crunch era.

Are we on a same page @balajithiks??

LikeLike

Agreed. Beyond a certain point, too strict a NPA rules invite short term behaviour and evasiveness what is counterproductive. Ultimately, what matters is the recovery of the loan for the lender, the LTV ratio, the soundness of the security etc.

LikeLike

Yes. In the past they had taken possession of the security and sold the same to recover the dues.

LikeLike