- Switzerland tried negative rates in the 1970’s and it got very ugly. (here)

- Unprecedented crisis in the financial sector, says NITI Aayog (here)

- Forget stocks, invest in stock exchanges (here)

- Amazon’s tiny profits explained (here)

- Buffett’s been quiet but his philosophy speaks volumes (here)

- Uber and Lyft take a lot more from drivers than they say (here)

Berkshire Quarterly Watch!

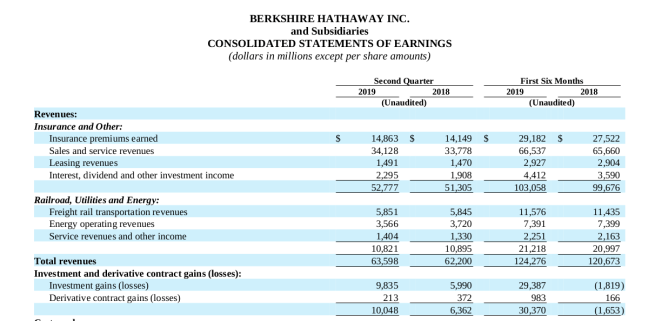

Berkshire Hathaway announced another solid quarter on Saturday. With unrealized investment gains flowing through its P&L, the results do incorporate wild swings in equities that needs to be accounted for while evaluating the results.

Revenue for Berkshire was up almost 2% YoY from $62.2B in 2018 to $63.6B in 2019. Investment gains were $10B in Q2 2019 compared to $6.3B in Q2 2018. Energy revenues were slightly down from $3.7B to $3.6B in Q2 2019. Insurance losses were sharply up from $9.4B to $10.7B or 13.8% on a much lower revenue growth of 3%.

The results do not include the Kraft Heinz results for the first half of 2019 as the results have not been announced yet.

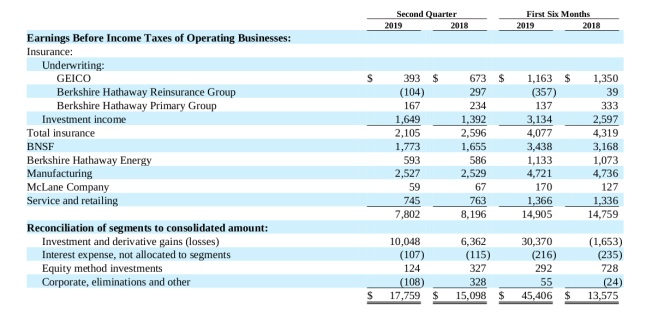

From an earnings perspective, significantly lower earnings from Geico, Berkshire Hathaway reinsurance and Primary group affected the overall operating earnings for Berkshire.

Berkshire continues to maintain a very conservative portfolio on the fixed income side with less than $20B compared to its $200B equity portfolio. It is a clear sign that WEB thinks that the bond market is overvalued and the returns do not justify the risk.

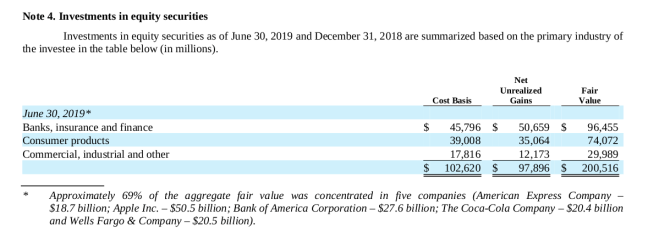

On the equity side, Berkshire sold more than it bought in the first six months and the cost basis remained roughly the same at $102.6B. Berkshire sold $4.6B of equities and bought around $2.8B in the first six months. The only notable news is that Wells Fargo continues to be a key part of the portfolio and BAC has now crossed the 10% ownership threshold for Berkshire. In the first six months of the year, $29.3B of net unrealized gains was recognized on the income statement.

Interestingly, the derivatives that Berkshire wrote before 2008 are starting to expire. Out of the notional exposure of $24B, over $10B will expire in 2019.

The buyback from Berkshire was also pretty lukewarm in Q2. $440M was repurchased in Q2 2019. With the cash balances further swelling to $122.3B, hopefully the repurchases will get more meaningful over time.

Brief thoughts on valuation:

Another robust quarter for Berkshire. Our thoughts on the valuation is a simple SOTP that many other value investors do. Berkshire can be divided into operating earnings of the business and the portfolio investments. Berkshire earned $10.8B pre-tax in their operating business (excluding insurance) in the first six months, with a run rate of $21.6B for the year. At a safe multiple of 10 given the robustness and the mix of the businesses, it amounts to $216B. I prefer to take the insurance earnings as zero given the cyclical nature of the business even though Berkshire has made profits very consistently. Portfolio investments at the face value of equity + fixed income + equity method investments and cash is approx. $358B. In total, the intrinsic value is about $574B with 2.452B B shares outstanding resulting in a conservative intrinsic value of $234 / B share.

Disclosure: Long BRK.B

Not a recommendation.

Berkshire Files with SEC on 10% ownership in BAC

We all know that Warren Buffett and Berkshire Hathaway have been bullish on banks in America. It looks like the fest is all set to continue. Berkshire Hathaway just filed a Form 3 with the SEC as a 10% owner of Bank of America (BAC). You can find the filing here

It looks like Berkshire has added over 54 Million shares in BAC since April 2019. What is even more interesting is that Warren Buffett and Berkshire have been actively selling down Wells Fargo every quarter for the last few years to keep its ownership interest below 10% (here) as it hampers their ability to do business with the bank (here)

It also looks like it is okay to own up to 25% of a bank as long the investor gets a permission from the federal reserve and assures them that they would remain a passive investor.

Whichever way you look at it, between WFC, BAC and the growing stake a JPM, Warren Buffett is owning a huge piece of the American banking system. And his actions are the strongest indicators on how Berkshire feels about the current valuation of American banks and areas where large amounts of capital can be deployed for Berkshire.

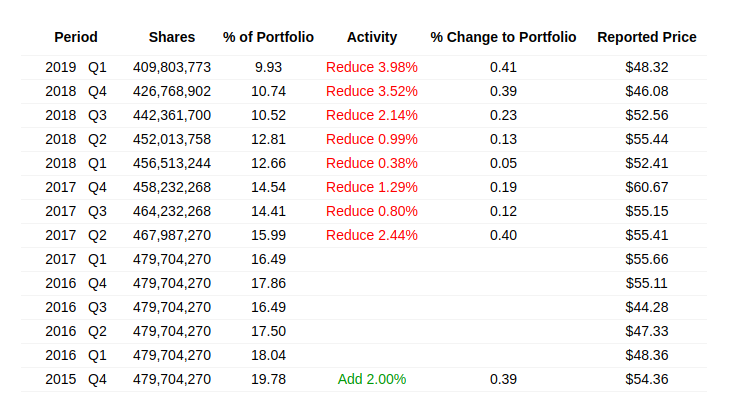

Wells Fargo (WFC)!

Wells Fargo has been a decisive name that has divided investors. While the fundamentals continue to hold steady, negative headlines and a rock bottom valuation continues to test the patience of investors. It has been interesting to look at what Charlie and Warren have been up to with Wells Fargo during this time.

Below is a look at the Daily Journal portfolio which is essentially managed by Charlie Munger. While the Daily Journal corporation is not the primary investment vehicle for Munger, it is hard to fathom Charlie not taking his fiduciary duty very seriously at Daily Journal on managing the portfolio.

Source: Dataroma (here)

The thing that caught my eye was just how big the Wells Fargo position is. It is over one half of the portfolio at this point. It is extremely interesting because Charlie has long preached assiduity and it looks like he is practicing it hard. Not a single trade on Wells Fargo since Q4 2013 (as far back as the database at Dataroma goes).

On the other hand at Berkshire, limited by an ownership limit of 10% that would force them to convert to a bank holding company, Warren Buffett has been selling just enough to keep it inside of the 10% ownership rule. While one can speculate on what would his actions if he was not loaded up to 10%, the act of keeping it just below 10% through this tough time for Wells Fargo is an indicator of the confidence that both Warren and Berkshire have on the bank.

Source: Dataroma (here)

Charlie Munger and Warren Buffett did weigh in on the Wells Fargo Issue a couple of months ago after the annual meeting at Omaha. It basically reinforces their faith in the bank while calling out the mistakes.

Some very interesting comments came from Saber Capital recently on Wells Fargo here

While it has been extremely interesting to watch the market react to the accounts scandal and politicians drum it up for headlines, what remains behind is a company that has $1.9 trillion in assets and $1.3 trillion in deposits that is buying back its shares and eating into itself. This year, an estimated 15% of the market cap of Wells Fargo will be distributed either in the form of a dividend or buybacks. Probably, it is not such a bad thing to be limited on growth but to allow the bank to buy itself back cheap on the back of negative headlines. While the headlines have been scary, the assets and the deposits are continuing to hold steady at Wells Fargo!

While time will tell how the next chapter unfolds but as an interested and a vested investor in Wells Fargo, it is tough to ignore the headlines and just watch the fundamentals. Probably time to practice some assiduity.

Short Post on Berkshire

While there are a lot of commentators out there commenting on Berkshire’s results, here is a short different take on it.

- In 2018, Berkshire took a pre-tax mark to market losses of $22.4B on investments and derivatives and $17.8B on a post tax basis

- Berkshire reinsurance group did not have a great year and lost $1.1B pre-tax driven by property casualty and retroactive reinsurance.

- Berkshire’s portion of the Kraft Heinz goodwill impairment was $2.7B in 2018

- $19.8B of Fixed Income securities compared to $172B of equities

- $109B in Cash and treasury bills

- Offset by strong earnings in the rest of the operating businesses and insurance companies resulting in a book value increase of 0.4% and net income of $4B for the year.

If on a year like this, Berkshire does not lose money, it talks a lot about the fortress balance sheet and the resiliency of the business model. I know that Buffett talks about not using BVPS any more. I look at it differently. It was an understated proxy for intrinsic value. Now, it is vastly understated for the intrinsic value.

It is often about return of capital before return on capital. There are a lot of commentary about Berkshire being an index fund. It might be but the risk profile is completely different.

What are we reading?

Blast from the Past: Timely reminder to think for yourself — Munger on Valeant

This is a dated post but fun nevertheless.

It all started in April 2015 when Valeant Pharma was the toast of town.

And then Charlie said this: “Valeant is like ITT and Harold Geneen come back to life, only the guy is worse this time.”

No one really understood what Charlie meant at that point. There were some speculations but no one was sure. This was way before the entire Valeant thing unraveled. Pause a moment to think. A lot of us had access to the same information and Munger came to a radically different conclusion than the rest of the market. Bill Ackman tried to reach out to Charlie and convince him otherwise here. Charlie turned out to be correct. How many times as investors have we had a radically different opinion than the rest of the market put together and been right? Are the markets always efficient? What qualitative factor is the market not pricing in that is not evident in the numbers?

In November in 2015, he explained himself further when Valeant started to come apart. Look at the initial response from Munger.

Later, of course, Munger ended up comparing Valeant to a sewer.

Here is how Valent played out finally. They now trade as Bausch Health Companies (BHC).

Now, Charlie also said Ackman was right on Herbalife; that has not proven out yet. Independent thinking….

What are we reading?

What are we reading?

Poll – Compete against Warren Buffett or Jeff Bezos

I am running a poll on twitter. Help Vote! Should be less than 10 seconds to vote!

Given a choice b/w building a eCommerce co or an Insurance conglomerate & compete with @WarrenBuffett or @JeffBezos Your pick? Poll below

— Beowulf (@beowulfcapital) January 8, 2017