Berkshire Hathaway announced another solid quarter on Saturday. With unrealized investment gains flowing through its P&L, the results do incorporate wild swings in equities that needs to be accounted for while evaluating the results.

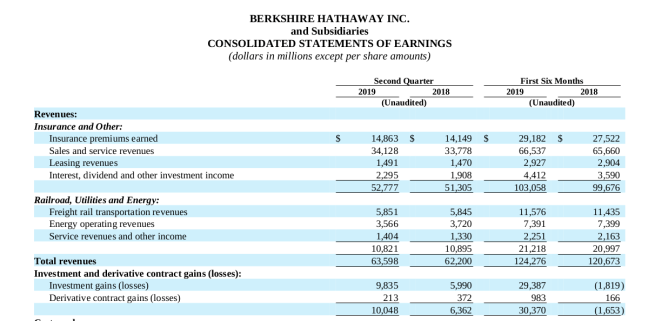

Revenue for Berkshire was up almost 2% YoY from $62.2B in 2018 to $63.6B in 2019. Investment gains were $10B in Q2 2019 compared to $6.3B in Q2 2018. Energy revenues were slightly down from $3.7B to $3.6B in Q2 2019. Insurance losses were sharply up from $9.4B to $10.7B or 13.8% on a much lower revenue growth of 3%.

The results do not include the Kraft Heinz results for the first half of 2019 as the results have not been announced yet.

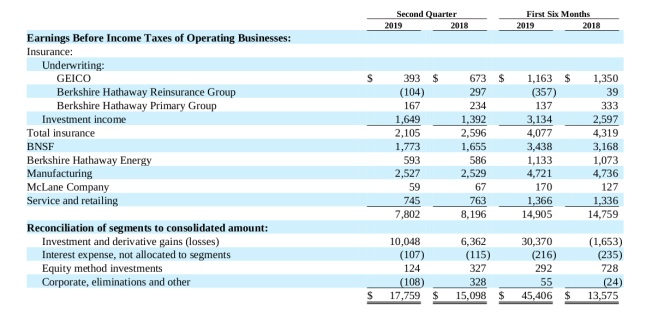

From an earnings perspective, significantly lower earnings from Geico, Berkshire Hathaway reinsurance and Primary group affected the overall operating earnings for Berkshire.

Berkshire continues to maintain a very conservative portfolio on the fixed income side with less than $20B compared to its $200B equity portfolio. It is a clear sign that WEB thinks that the bond market is overvalued and the returns do not justify the risk.

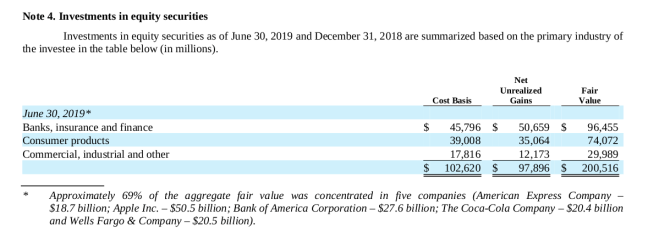

On the equity side, Berkshire sold more than it bought in the first six months and the cost basis remained roughly the same at $102.6B. Berkshire sold $4.6B of equities and bought around $2.8B in the first six months. The only notable news is that Wells Fargo continues to be a key part of the portfolio and BAC has now crossed the 10% ownership threshold for Berkshire. In the first six months of the year, $29.3B of net unrealized gains was recognized on the income statement.

Interestingly, the derivatives that Berkshire wrote before 2008 are starting to expire. Out of the notional exposure of $24B, over $10B will expire in 2019.

The buyback from Berkshire was also pretty lukewarm in Q2. $440M was repurchased in Q2 2019. With the cash balances further swelling to $122.3B, hopefully the repurchases will get more meaningful over time.

Brief thoughts on valuation:

Another robust quarter for Berkshire. Our thoughts on the valuation is a simple SOTP that many other value investors do. Berkshire can be divided into operating earnings of the business and the portfolio investments. Berkshire earned $10.8B pre-tax in their operating business (excluding insurance) in the first six months, with a run rate of $21.6B for the year. At a safe multiple of 10 given the robustness and the mix of the businesses, it amounts to $216B. I prefer to take the insurance earnings as zero given the cyclical nature of the business even though Berkshire has made profits very consistently. Portfolio investments at the face value of equity + fixed income + equity method investments and cash is approx. $358B. In total, the intrinsic value is about $574B with 2.452B B shares outstanding resulting in a conservative intrinsic value of $234 / B share.

Disclosure: Long BRK.B

Not a recommendation.