Berkshire Discloses Ownership in Kraft Heinz (Valuewalk)

Moody’s corp. Long idea (jInvestor)

Railroads Competitive Advantage are Solid but Challenges Lay AHead (Morningstar)

Do Something Syndrome (Farnam Street)

Berkshire Discloses Ownership in Kraft Heinz (Valuewalk)

Moody’s corp. Long idea (jInvestor)

Railroads Competitive Advantage are Solid but Challenges Lay AHead (Morningstar)

Do Something Syndrome (Farnam Street)

Charlie Munger: The Psychology of Human Misjudgement (Farnam Street)

Media Consumption (Farnam Street)

Buffett’s Kraft Heinz Bet Valued at $24B on Debut (Bloomberg)

Our Post of Kraft Heinz (Here)

About a week ago, Molycorp, the rare earth minerals manufacturer declared a chapter 11 bankruptcy.

From google finance,

Molycorp, Inc. is a rare earths producer. The Company operates in four business segments: Resources, Chemicals and Oxides, Magnetic Materials and Alloys and Rare Metals. The Resources segment includes its operations at the Mountain Pass facility. The Chemicals and Oxides segment includes the production of rare earths at Molycorp Silmet; production of separated heavy rare earth oxides and other engineered materials from its Molycorp Jiangyin facility, and production of rare earths, salts of rare earth elements (REEs), zirconium-based engineered materials and mixed rare earth/zirconium oxides from its Molycorp Zibo facility. The Magnetic Materials and Alloys segment includes the production of Neo Powders through its wholly owned manufacturing facilities. The Rare Metals segment produces, reclaims, refines and markets niche metals and their compounds.

Often companies get into bankruptcy as they are unable to absorb the burden of the debt that they have undertaken and go through the bankruptcy process and come out stronger with better negotiated debt on the other side. The market that Molycorp operates in is dominated by Chinese firms . When the economic behemoth tried to strong arm the world by controlling supplies, Molycorp and Lynas came up with supplies with some non-Chinese mines. These two companies at one point contributed to 10% of the global consumption. Since then the Chinese have backed down and the world has been more than willing to buy from them at rock bottom prices.

When one looks at the financials of Molycorp, attention needs to be paid to the income statement rather than the balance sheet as we usually do in distressed conditions.

| $M | 2012 | 2013 | 2014 |

| Sales | 527.7 | 554.4 | 475.6 |

| GP | 18.8 | -67.2 | -99.6 |

| GP % | 3.6% | -12.1% | -20.9% |

The company has been reporting net negative gross margins. The company has been losing money just getting metal out of the ground. This is even before the sales force is paid, the corporate expenses are paid and even before the interest payments are serviced on the debt. The only time when the GP’s were positive was during the Chinese induced shortages which resulted in a huge price increased in the market. Just restructuring the debt with lower interests or better terms or financial engineering is not the solution to this problem.

The company has not outlined any measures that can make the investor comfortable that a margin of safety exists in the bond even under distress. Unless there is another attempt to strong arm the rare earth market from the Chinese or the US is determined to use only US made rare earth metals, or the Chinese crack down on the black market, financial engineering will only go far to stem this tide. A cautious investor will do well to sit this out and watch from the sideline!

Charlie Munger compares Greece to Drunken, Frivolous Brother-In-Law (ZeroHedge)

The Greek Exodus in One Chart (ValueWalk)

Three Links for a good Career (@Sanjay_Bakshi)

The uncanny similarities between IndiGo and Jet IPO’s (Mint)

In a rebuke to Europe, Greece votes no to bailout terms (WSJ)

What does Europe look without Greece (WSJ)

Simply knowing isn’t enough to change behaviors (FarnamStreet)

The evolution of a value investor (ValueWalk)

Heinz completes Kraft Merger, Buffett to Join Board (NYTimes)

Our previous post on Heinz Kraft merger and our thoughts (here)

Warren Buffett re-examines Re-Insurance (WSJ)

The education of AirBnB’s Brian Cheksey (Fortune)

How Shelby made $900M in Insurance (Valuewalk) H/T: AlphaIdeas

Be Skeptical; Mantri Developers Assures 100% Return Again with SEBI and RBI watching (capitalmind) H/T: Alphaideas

Persistent Systems: Globetrotter (Persistent)

Emerson Electric to spin off the network power business (WSJ)

How Greece went Bust (Reuters)

ACE to buy Chubb for $28B (WSJ)

China’s most formidable startup is expanding outside Asia (BusinessInsider)

Fascinating facts about best selling products (BusinessInsider)

The biggest mistake investors make with options (ValueWalk)

From Google finance:

Sysco Corporation (Sysco) along with its subsidiaries and divisions, is a North American distributor of food and related products primarily to the foodservice or food-away-from-home industry. The Company provides products and related services to approximately 425,000 customers, including restaurants, healthcare and educational facilities, lodging establishments and other foodservice customers. Sysco provides food and related products to the foodservice or food-away-from-home industry. The Company has aggregated its operating companies into a number of segments, of which only Broadline and SYGMA are the main segments. Broadline operating companies distribute a line of food products and a variety of non-food products to their customers. SYGMA operating companies distribute a line of food products and a variety of non-food products to chain restaurant customer locations. The Company’s other segments include its specialty produce, custom-cut meat and lodging industry products segments

Sysco was recently in the news for terminating the merger deal with US foods (link here). At the same time they announced that they would be buying back stock of about $3B from the market.

Let us see what happens as a result of this buyback. For the sake of simplicity, let us assume that Sysco can buyback the stock without significantly influencing the price.

| Sysco current price | 37.54 |

| Oustanding shares | 599 |

| Buyback ($M) | 3000 |

| Shares to be repurchased | 79.91476 |

| After buyback outstanding shares | 519.0852 |

| Net Income | 868 |

| EPS before buy back | 1.449082 |

| EPS after buy back | 1.672172 |

| % EPS Growth | 15.4% |

So far so good. Current investors can spend $3B at current prices and get a 15% bump on EPS.

Any company can spend the money it generates in four ways

At any given point, the CEO, whose prime job is capital allocation, is deciding where to allocate the money.

The current ROE of Sysco is 16%. Let us explore option 4 and see what happens if Sysco is able to generate half the ROE that it generates with the new programs on which it would spend the $3B on without diluting shares by using internal cash generation and debt to generate an incremental ROE of 8%.

| To be invested in additional internal project ($M) | 3000 |

| ROE | 8% |

| Additional to FCF and Net Income / year (simplified to assume the same number for both) ($M) | 240 |

| Net Income after re-investment ($M) | 1108 |

| EPS | 1.84975 |

The EPS growth in this case is 27% significantly higher than the buyback scenario. The ROE of internal projects needs to be 4.4% for the buyback option to make sense over the re-investment scenario which is also a possibility and we can assume that the CEO has done his due diligence.

The questions that begs to be asked are as follows:

Not all buybacks are created equal. A conservative investor needs to be cautious before rewarding businesses blindly that buyback shares in the name of shareholder value creation.

Molycorp creditor Oaktree scores with savvy move (WSJ)

Caught in the big sale (BusinessWorld)

Remember the Nifty Fifty (USAToday)

United Bank tops the list of banks with bad loans among PSU banks (MoneyControl)

Greece saunters across the autobahn (Bloomberg)

Why the CEO of Coca Cola never dines alone (Fortune)

Disney’s strategic vision (Valuewalk)

BIS warns of next financial crisis (Valuewalk)

More often than not, alpha is created from the ability and testicular fortitude to say no 99% of the times rather than our ability to say yes.

— Beowulf Capital

As per DNB’s 10-K (2014)

The Dun & Bradstreet Corporation is the world’s leading source of commercial data, analytics and insight on businesses. Our global commercial database as of December 31, 2014 contained more than 240 million business records. We transform commercial data into valuable insight which is the foundation of our global solutions that customers rely on to make critical business decisions.

Below table shows the underlying EPS change adjusted for buybacks.

| 2010 | 2011 | 2012 | 2013 | 2014 | |

| Shares Outstanding | 50.4 | 49.3 | 46 | 39.5 | 36.9 |

| -2.2% | -6.7% | -14.1% | -6.6% | ||

| Theoretical Net Income | 50.4 | 50.4 | 50.4 | 50.4 | 50.4 |

| EPS | 1 | 1.02 | 1.10 | 1.28 | 1.37 |

| Actual Net Income | 252 | 260 | 296 | 259 | 294 |

| EPS | 5.0 | 5.3 | 6.4 | 6.6 | 8.0 |

| EPS change | 5.5% | 22.0% | 1.9% | 21.5% | |

| Underlying EPS change | 3.2% | 13.8% | -12.5% | 13.5% |

The underlying business shows strong improvements in the underlying EPS except for 2013.

This is a very interesting case where so far we have seen shows a very strong underlying business. It is almost a Warren Buffett type of company.

Let’s look at the entire business from another perspective

| $M | 2010 | 2011 | 2012 | 2013 | 2014 | 4 Year CAGR |

| Revenue | 1677 | 1759 | 1663 | 1665 | 1682 | 0.1% |

| Gross Profit | 1119 | 1171 | 1142 | 1105 | 1112 | -0.2% |

| Operating Profit | 409 | 425 | 432 | 437 | 422 | 0.8% |

| Net Income | 252 | 260 | 296 | 259 | 294 | 3.9% |

So, revenue, gross profits and operating profits have not moved at all in the last four years so where is all the underlying EPS change coming from?

| % | 2010 | 2011 | 2012 | 2013 | 2014 |

| Tax Rate | 35.55 | 29.67 | 21.97 | 34.22 | 15.09 |

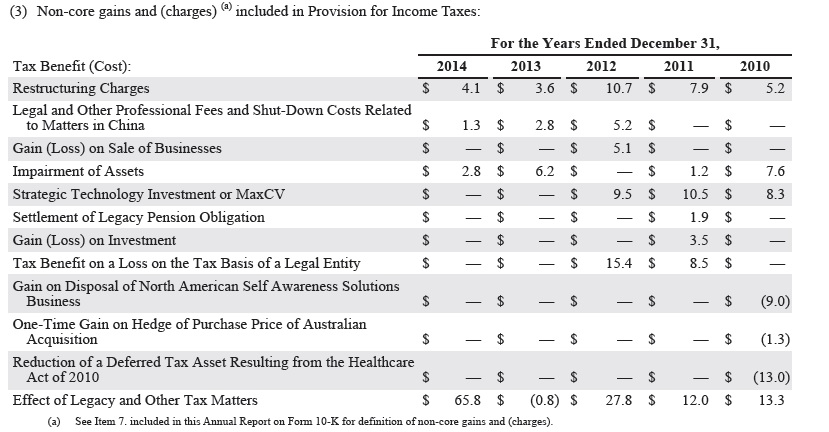

2013 EPS was -ve when DNB paid a full tax rate and 2014 EPS growth was all driven by lower tax provisions. So, what is driving this different tax rate? In page 140 of the 2014 annual report is the answer.

in 2013, when the company had no tax benefits from restructuring or legacy tax matters, the tax rate was full 35%. The underlying EPS change was (12.5)%. There was a $66M legacy tax in 2014 without which might not be available in 2015 and forward. So, what was driving the $66M legacy tax benefit?

It definitely looks like a non-recurring tax benefit. The company does however comments that it might benefit from more sales into lower tax states but does not quantify the same. Can a conservative investor count on tax benefits to help drive free cash flow in the future?

A zero sales growth, negligible operating profit growth and free cash flow growth company is trading at 19 times earnings in the US… With competition intensifying from low cost search aggregators and a changing landscape in technology services, Investing in DNB today does look like a very speculative bet. While the underlying business drives strong ROE and has great products, a shareholder investing in the common might not see the benefits of the same in the long run.

Disclosure: No position