Fairfax is a global P&C insurance company led by its charismatic CEO, Prem Watsa, often dubbed as the Warren Buffett of Canada. Fairfax has compounded book value by 20.4% CAGR since inception and the stock price has closely followed it at a 19.4% CAGR. However, the recent performance has been anemic and events have left a lot of questions unanswered about Fairfax.

Picture Source: 2015 Fairfax Annual Report

Fairfax Macro Position:

Fairfax has had a long history of making bold macro calls and producing returns for its investors. The most recent successful macro bet was during the great financial recession between 2007-2009. Fairfax was early in the macro call before the recession but profited handsomely when shocks permeated through the financial world.

Source: 2013 Annual Report

Coming out of the recession in 2010, Fairfax saw similarities between the 2008 recession and the 1929 depression and took a position based on the assumption that the recession story had not been completely played out. Fairfax took a bearish stance in two different ways, through derivatives linked to CPI’s and equity hedges on its portfolio. The CPI linked derivatives have been covered extensively in several places and is a key component to the bullish thesis on Fairfax. However, these are not the securities that have caused the under performance. It is the equity picks of Fairfax.

As we will see later, the under performance on the equity picks meant that the equity hedges kept Fairfax in a net short position in a bull market over the last several years.

Book Value per Share:

The book value per share compounded 2.6% CAGR between 2011 and 2015 for Fairfax. This can be separated into two different components. The shareholder’s equity has been compounding at 4.8% CAGR and the shares outstanding has been diluting at 2.1% CAGR over the last five years resulting in a net compounding of 2.6% over the five year horizon.

As with most insurance companies, Fairfax’s economic engine is driven by

- A profitable insurance underwriting company that generates benefit of float and a great capital structure,

- An investment portfolio consisting of bonds and stocks to generate leveraged returns for shareholders

Insurance operations at Fairfax:

Fairfax has a decent record of underwriting over the last five years. The company’s insurance operations have generated $954M of underwriting profit over the last five years. The insurance operations provides a capital structure that enables Fairfax to borrow cheaper than the government of Canada and get paid to hold the premiums in advance. As the tailwinds in the insurance markets continue, Fairfax will continue to benefit out of this. The capital structure is a great source of competitive advantage for insurance companies. I would like to cast the readers attention to our article on capital structure some time ago here.

Investment Returns at Fairfax:

When one looks at the net result of realized and unrealized gains at Fairfax from 2011 to 2015, one would notice that the equity investments have lost Fairfax $378M over the last five years. This mediocre performance has been driven by the under performance of the equity that Fairfax has invested in as compared to the strength of the bull market in general over the last five years. In addition to this, the CPI linked derivatives have cost another $436M to shareholders. However, given the extreme pay off ratio if some of these bets do realize probably makes them a speculative risk worth considering given Fairfax’s long term macro record.

At the end of 2015, the value of market investments for Fairfax was about $650M below the cost of the investments. This is before any equity hedges or derivatives causing further deterioration. The common stock exposure (below table excludes funds that are common stock investment funds that primarily has fixed income bonds) shows that close about 40% of the common stocks are held in the US and Canada. There is a significant exposure to stock markets in Greece, Egypt, Ireland, India, China and Kuwait. This is not something for the fainthearted. There are two ways to look at this, the brighter side is that these markets could be a source of alpha, and on the less brighter side, these could result in a host of political, volatility and currency risks.

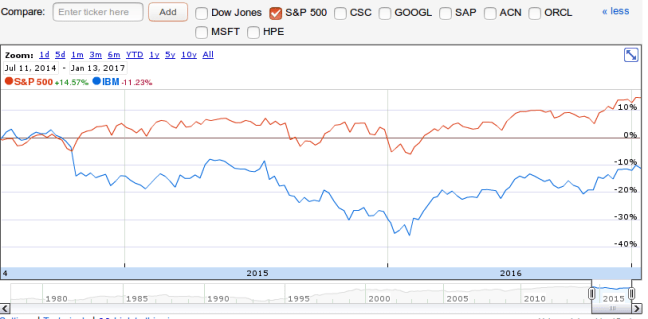

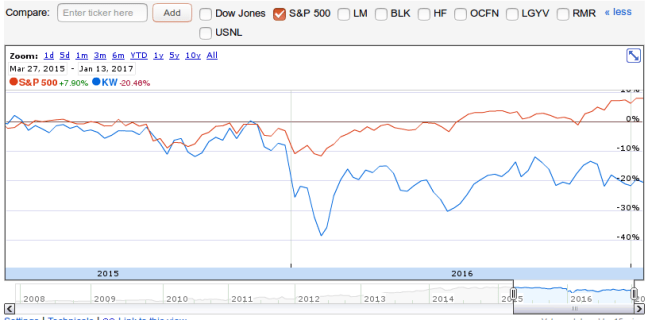

We looked through the most recent 13-f filings for Fairfax’s performance of its long positions in the US.

The four positions in the US make up around 83% of the reported US equity portfolio. Their performance has not been inspiring. We looked up the buying period when Fairfax added these positions and their relative performance against the S&P 500.

In addition, we reproduce the below extract from the annual report for one of the biggest Greece investments for Fairfax.

The under performance of the equity picks from Fairfax as against the Russell and the S&P index has caused erosion in the value of the investments for Fairfax. Instead of hedging against equities, the poor long picks of Fairfax has landed them in a net short position that caused them to lose money ($377M) against the general market.

These risks continue to exist in Fairfax stocks today. After the recent election results, the equity hedging has been reduced to 50% from the 112% at the end of Sep, 2016. Unless the underlying picks start performing better, the returns from the equity side will continue to be anemic. The foreign markets risk is something a prudent investor must think carefully over before investing in Fairfax.

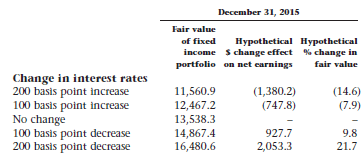

The bond portfolio:

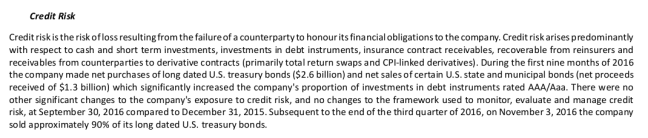

With the great disconnect in mind, Fairfax piled on bonds in the anticipation of lower interest rates. With the recent interest rise hikes and the anticipation in the future, one needs to closely look at the duration of the bonds at Fairfax.

Close to half the bonds held at Fairfax have a maturity greater than 10 years which is result in interest rate sensitivity being high on the bond portfolio.

Contrast this with Berkshire Hathaway where less than 10% of the bonds was have duration greater than 10 years.

Source: Berkshire Hathaway 10-K 2015

Correction: Subsequent to Q3, Fairfax sold 90% of long dated US treasuries which is about $5.6-$5.7B of Bonds. It will be interesting to see the use of cash subsequently as another source of profits in the last few years has dried up.

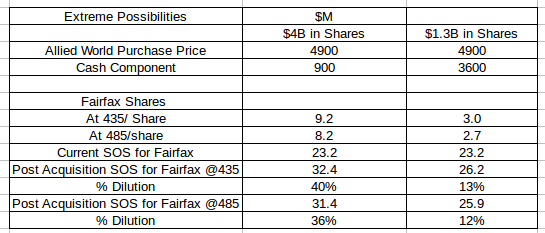

Allied World Acquisition:

Fairfax announced the acquisition of Allied World for $4.9B or $54 per Allied Share. $10 of dividend from the cash between Fairfax and Allied World and the rest in the form of Fairfax shares. Essentially, $0.9B of cash between Fairfax and Allied and then $4.0B of Fairfax stock with an option to replace $2.7B of stock with cash within 75 days of the announcement. It was very interesting to see the conference call where it was announced that Allied would be decentralized and there are no cost synergies. So essentially Fairfax is paying between $435 and $485, a share implying a book value of 1.07 to 1.19 (9/30 2016 BVPS) to buy a company at 1.35 times book value.

Source: Allied Acquisition Slides

Okay. Here is an excerpt of the intrinsic value of Fairfax from the 2015 annual letter.

So, essentially, Fairfax took undervalued shares to buy Allied World at 1.35x book without any cost synergies. I do hope that Fairfax understand what they are getting in return. Given the long duration bond portfolio and the lackluster performance of the equity book, the additional float for investment cannot be solution to the problem. The current shareholders are going to be diluted anywhere between 12% and 41% through this acquisition.

All the recent events and their performance raises more questions than answers. As a long term holder of Fairfax, I have to re-think a lot of the assumptions about Fairfax and this post is part of the evaluation. Any new buyers, caveat emptor.