We had blogged about Discovery communications before here. On March 20th, the stock closed at $16.87 / share with 711 fully diluted shares outstanding generating a market cap of ~$12B. The company carries debt of $15.4B. The company also generated operating cash flow of $3.4B with a net income of $2.069B in 2019. Capital expenditure was $0.3B and interest payments were $0.7B. Since Discovery always plans to carry a debt load of 3-3.5X, it might be wise to assume the interest payment stays for ever, the FCF adjusted for interest payments is $2.4B. The company is trading at 5 times adjusted FCF and 10 adjusted FCF to market cap.

There are two basic questions that we need to probe further.

a. Is there any possibility of running into liquidity issues or rolling over debt for the company?

b. Effect of Coronavirus and its implications for the company?

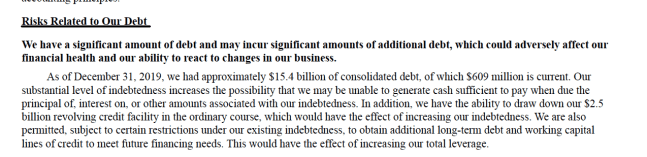

Debt position: Since Discovery has $15B of debt on its book, it might be worthwhile to see the amount that might come up for renewal in the near future. As seen below, $600M of 2.8% senior notes are coming for renewal in June. $600M in 2021 and close to $1.2B in 2022.

It is clear that the company can cover the interest principal payments very well with internal cash flow even if they are not able to tap the capital markets in 2020 and 2021. Liquidity and capital positions look solid from that point of view. Unless the cash flow falls completely off the cliff that would put the debt covenants in default, it looks like Discovery might be well placed.

Covid impact: On one hand, since the entertainment options for people have reduced in the last few weeks due to Covid, it is possible it might be a positive for the company. However, given the economic crunch that is sure to follow, one must consider whether the cord cutting will accelerate costing subscribers and a permanent FCF reduction to Discovery. This will be a function of the length of the slump and it is too early to call that. I have no insight except that the markets have priced in a massive slump and China and Korea recovered in a 2-3 months.

Discovery also had rights to broadcast Olympics in some countries but the CFO came out at the end of Feb and said that the financial impact would be minimal in case of a Olympics cancellation. In addition, the company holds insurance against cancellation.

With $1.6B of cash, $2.5B of accessible credit facilities, strong FCF generation YTD, a manageable debt to extinguish over the next 12-24 months, the company seems to be unnecessarily priced to extinction. Unless the economy turns into a depression type scenario, the unique content of discovery communications, coupled with the strong financial cushion allows it to weather short short term shocks well. It sure looks like a case of Mr. Market voting the company down in the short term creating interesting possibilities for cash rich investors.

Disclosure: Own DISCK

{kind=link}