Note: I have used a lot of approx. calculations as a proxy to quickly look through DISCA/K’s numbers.

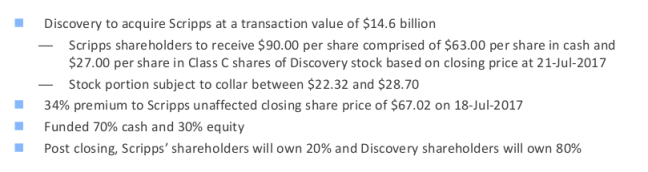

Discovery Communications (DISC(A/K)) entered into a merger agreement with Scripps Networks on July 31st, 2017. Discovery will pay $90/share to Scripps shareholders in a combination of cash and stock. The transaction is expected to close in Q1 2018. Below outlines the transaction details on how Scripps SH will get paid.

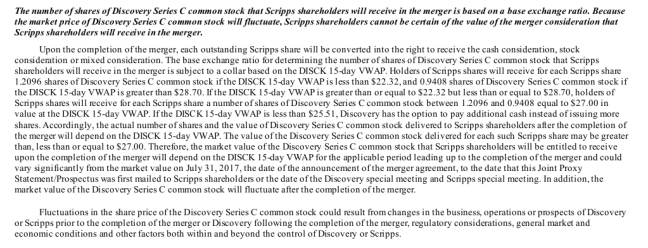

Furthermore, the amount of Discovery stock that Scripps will get paid depends on the 15 day VWAP of Discovery shares before the close.

Essentially, if the 15 day VWAP is less than $22.32, Scrips SH will get paid 1.2096 shares of DISCK; if 15 day VWAP of DISCK > $28.70, then 0.9408; if 15 day VWAP of DISCK between $22.32 & $28.7, then it will be the 15 day VWAP averaging to $27.

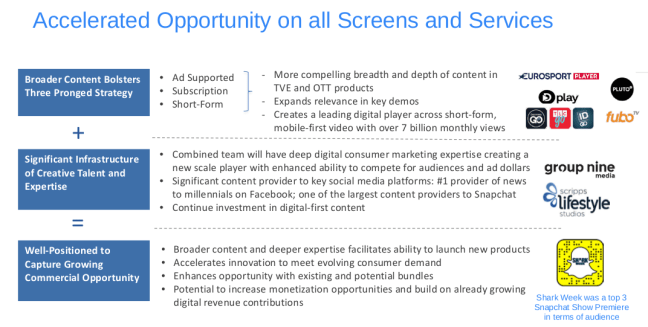

The strategic rationale explained by Discovery for the acquisition was to create a scaled up independent media company. Discovery will own 0.3M hours of programmable content with 8K hours being produced annually between the two networks. The potential for Scripps to grow outside the US will provide top line synergies while the cost synergies are expected to be around $350M annually. The two companies together will account of 20% of ad supported paid TV network in the US.

The combined network of discovery and Scripps is shown below.

Top line & bottom line synergies are shown below:

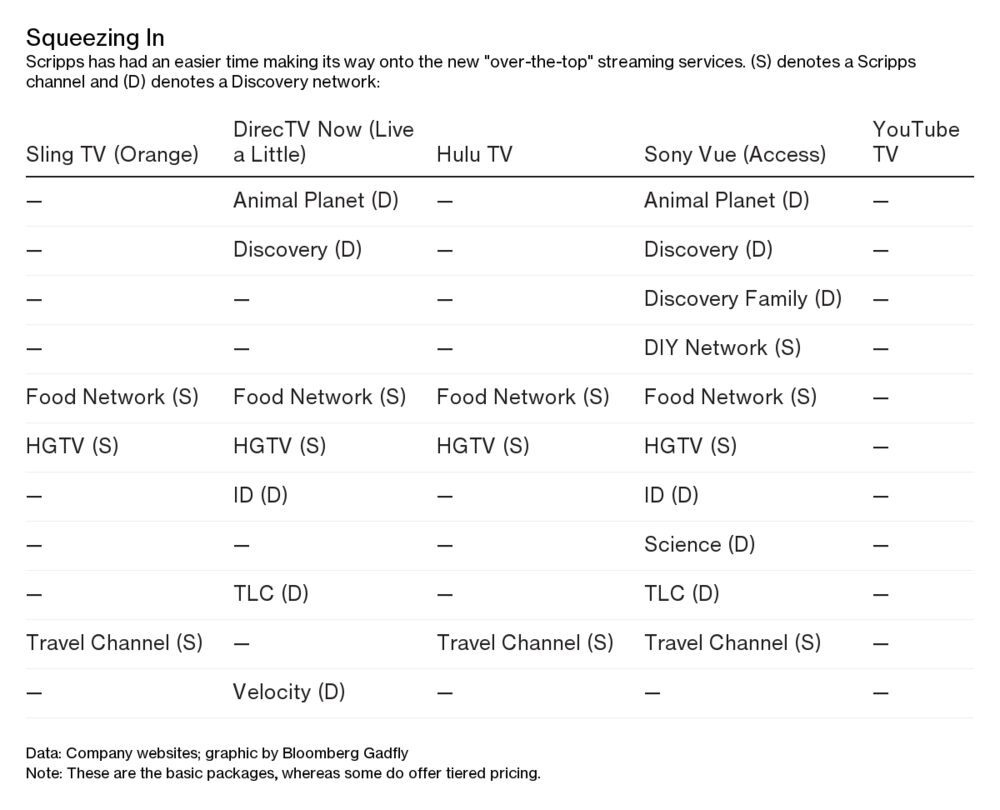

Since the acquisition has been announced, DISCK has been on a slide clearly indicating the market’s reaction to the deal and the fact that Discovery is losing subscribers at the rate of 3% a year and 5% in the recent quarter driven by its smaller network. The Scripps deal will give it faster access to the skinny bundles / OTT as shown here by Bloomberg. (Article link here)

The stock is in doldrums crashing to low of $15/share and currently trading at $16.46/share. DISCK was trading close to $26/share at the time of the announcement of the merger.

The key reason behind this crash seems to be the suspension of buybacks in order to fund the merger, dilution, higher indebtedness and the industry fears of cord cutting and Discovery’s move to double down on the pay TV video model.

So, how does DISCK plan to pay for the $63/share to Scripps shareholders?

The additional $8.6B meant that DISCK has to suspend buybacks till it pared down debt to manageable proportions (3.5X OIBDA as stated during the transaction). The expected leverage at the time of closing is 4.8X. Going by the playbook of John Malone, at 3.5X, it will be a debt that will stay on the books forever and then the buybacks will start again. Before they start buying back stock, Discovery will have to retire $6B+ worth of debt.

Let us take a look at how the two companies put together look like (using full year 2016 numbers)

At first glance, one would wonder why would you put together two companies that are making $1.8B/year separately into a merger to generate $1.0B?

A closer look reveals that combined NI is $1.06B. Because of the huge premium paid, the D&A will shoot up. This is part of the price being paid to acquire intangible assets of Scripps and will be amortized. When you look at Capex for Discovery and Scripps, combined they do not spend more than $200M.

NI + D&A – Capex = $1.06B + $1.57B – $0.2B = $2.4B over 770 million SOS. A good proxy for owner’s earnings. See below tables for calculation on the SOS.

So what happens to the increased debt and taxes? Interest expense goes up and taxes come down. The additional debt is at weighted average of 3.6% and additional $316M of interest expense is offset by $506M of income tax savings. If there is further reduction in the tax rate, that would be an additional cherry on the top. Further, the cost synergies of $350M will translate to approx. $100M in year 1 and approx. $200M post tax dollars starting year 2 and drive both cash flow and the NI to grow.

$2.4B + OIBDA Growth (Assume 10% year year initial two years from sales synergies) + Cost synergies growth ($100 1st year, $200 second year), Discovery & Scripps combined will generate $2.7B and $3.2B in year 1 and 2 or $9.5B in first 36 months.

At 770 M shares (post dilution) at $17/share, the market is valuing Discovery at $13B or at 5.5 times owner’s earnings. The market has priced Discovery for failure. If they succeed in realizing the synergies, it will be a blockbuster stock. If they manage okay with the integration, it will still be a great bet with acceptable returns.

Even though Discovery is losing subscribers, it is growing its OIBDA every year and with the Scripps merger, it will greater access to the OTT market. Discovery’s international platform will also benefit Scripps. Currently, the market is pricing Discovery Communications to be dead in the water. It will be interesting to see how this plays out.

Disclosure: Not to be taken as investment recommendation. Might trade in DISCA/K

Sources for this post: S-4 Form, Merger Presentation, 10-Q’s

{kind=link}