When STFC had released their annual results and the Q4 numbers, I had written the following post after looking at the provisions for the Shriram Equipment Finance division. Now, their annual report was released and as with most longs I have, I did read through the report over the weekend.

In 2015 compared to 2014, NIM on AUM remained very strong at 6.61% versus 6.68% prior year. Despite the additional INR 325 crores of provisions in 2015 in the Shriram’s equipment subsidiary, and the total provisions increasing by 28% to 1,612 crores from 1,213 Crores in 2014, the company reported net profits north of INR 1,000 crores. On the balance sheet, there is still INR ~1,800 Crores already provisioned waiting for assets to go bad and paid out.

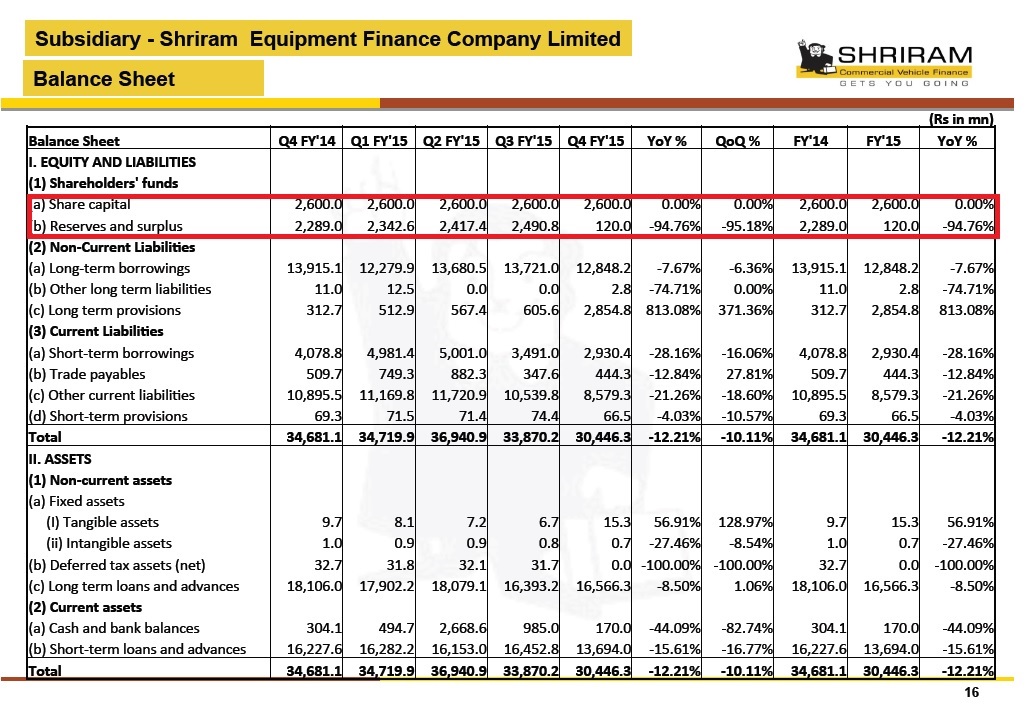

Interesting was how little the subject of write off in the equipment business got a mention in the main annual report of STFC.

The total AUM is up to 62K Crores from 52K Crores. Diluted EPS is down to INR 45 from 59 in 2014. The company earned 1,022 Crores in 2015 compared to 1,357 in 2014. Rest of the things were boilerplate with the expected recovery in the economy and the commercial vehicle market expected to drive higher earnings but it does look like the long term story does look intact.

The one thing that caught my eye was note 22 in the annual report.

For the company to start losing money or book value to start going backwards close to 2,600 crores or close 4.5% of its book must go bad at the same time every year. Even after that, the company has sufficient reserves and a high CAR to take pain for a while before it would start bleeding bad. Assuming that the company has taken the bloodbath in the equipment finance arm, one can expect to see some improvement in the consolidated EPS but looks like recovery in the economy might be a while away and the company might continue to struggle on the NPA’s on the main transport finance business.

As we have iterated in the past, a good economic moat surrounds the business, with a management that is conservative and has demonstrated integrity in the past, though in a cyclical business. The long term story does seem to remain intact.

Disclosure: Long STFC