When Charlie Munger speaks, it pays to listen. Hat tip to @valuewalk we can read through the full notes from the $DJCO 2015 meeting. As always, Charlie’s thoughts are profound and candid as always. Here is the link to the annual meeting notes.

What are we thinking?

We are thinking quietly about the Kraft Heinz deal. What is the hidden margin of safety that Buffett is counting on?

When we look back on Berkshire’s acquisition of BNSF, the deal initially looked crazy. Here is Warren’s justification for it and here is what some of the value investors thought about it. Investors believed that Warren had gone loco. The deal turned out to be very good for Berkshire shareholders. Five years since the deal, BNSF has provided $15B dividends back to Berkshire on the purchase price of $26.5B that he paid to own the rest of the company. (Link) Part of that was luck due to oil being transported more on rails compared to five years ago that even Warren could not have anticipated. Nevertheless, when Warren has capital of tens of billions of dollars that needs to get allocated, he is still finding deals with the required margin of safety and returns proving that he is a continuous and an innovative learner. If one were to value the railroad at where the competitors are trading it, it looks like BNSF will be worth about $66B.

One has to sit back and think about what are the margins of safety is Warren counting on the Kraft-Heinz deal? One, of course is 3G’s focus on cost. But is there something beyond it? What does it mean for the Shareholders? It will be the second biggest security in the Berkshire’s portfolio soon.

What are we reading?

Markel Ventures by Brookyln investor here

Markel 2014 Annual Report Analysis by Brooklyn investor here

Kraft Heinz Deal by Brooklyn Investor here

Why the Kraft Heinz Deal is a Rare Kind of Warren Buffett Deal by Forbes here

Wall Street is Feeling Left Out after the Kraft Heinz Deal by Business Insider here

The contrarian insurance play — Fairfax Financials 2014 Letter

Fairfax Financials, run by the contrarian CEO, Prem Watsa, continues to be bearish on the prospects for the world economy and Fairfax is backing his conviction with a very big bet on CPI linked contracts. While the world continues to be riveted on the statements of the Fed and is expecting a rate hike in the near future, Fairfax bets seem to question the sustainability of the hikes. Recent comments from Bridgewater chief, Ray Dalio, seems to the only other prominent voice echoing similar sentiments.

Fairfax had a good 2014, as is the case with most insurers, primarily driven by lack of catastrophes. Book value increased 16% to $395. Combined ratio was 90.8% and the company ended with $11.7B of float. Unrealized gains from bonds held in the investment portfolio contributed $1.1B of gains and drove the net earnings number higher in 2014. A closer look at the performance of the investment portfolio shows a mixed picture. The equity hedges has cost the company a pretty penny and almost all of the gains have come from the bonds portfolio.

Fairfax’s bet on bonds has spectacularly paid off while its equities have severely underperformed the market primarily driven by hedging. Prem Watsa and his team seem to be very confident about the market unravelling due to the grand disconnect between fundamentals and stock prices. It is worth noting that ten years ago, Prem Watsa had placed a similar bet on the housing market and suffered through initial years of losses before spectacularly reversing the losses during 2007 and 2008 as seen below. Only time can tell whether Fairfax will gain spectacularly on these CPI linked hedges.

If one digs a little deeper into this, the cost of these contracts seem to be only 7% of equity. On the surface, it looks like a bet where the payoff is huge with minimal downside risk. Currently, they have a string of loses to show for the bet between the CPI linked contracts and the equity hedges. Cumulatively, it has cost Fairfax Shareholders close to $4B to keep this bet on.

Furthermore, Fairfax is increasing the size of the CPI linked bet on deflation. The notional amount is now $111B. CPI seems close to the strike price and for the first time, the bets looks like having any chance of making money for shareholders.

So far so good. However, if inflation does occur like the rest of the investment community believes in, Fairfax stands to suffer from a triple whammy. Firstly, the loss from the CPI indexed contract. Secondly, the gain on equity will be minimal due to the hedges involved if the market does not unravel. Thirdly and most importantly, the bond portfolio might come under attack. Fairfax would still retain the option on holding the bonds to maturity and redeeming them but will have to announce mark to market losses in the meantime.

In net, Fairfax seems to be riding the wave of good underwriting profit along with most of the good insurers. The future seems to be hinged on the great disconnect in the stock markets. Only time will tell whether there the grand strategy will pay off or will it result in a lost decade for the insurer.

Disclosure: Long Fairfax

Markel 2014 Year End Letter

Markel Corp. is arguably one of the world’s leading insurance operator. It has one of the best track records in the insurance business with a very conservative management, accounting practices and a business model that is evolving to the size the Markel is growing to. We purchased Markel on the days after the acquisition of Alterra, when for a brief few days, the shares traded at book value. Since then, we have been sitting on it.

As seen below, Markel has had a stupendous year, with both book value and the 5-year CAGR both doing pretty well. The 5 year book value CAGR is a good indicator for long term value creation for balance sheet driven companies. By and large, the letter is all good news.

There is one painful section of the letter that I had a tough time comprehending — Markel Ventures. Markel has been on the tested path of Berkshire Hathaway, to own operating companies as an alternative capital allocation vehicle to investments. By and large, it has been fairly successful. Compared to ten years ago, the revenue has growth from $60M to $800+M. However, it was the discussion about EBITDA that caught my attention. Markel Ventures is measured based on adjusted EBITDA. EBITDA as a metric is bad enough but the metric goes even further and excludes goodwill impairment charges. The letter then goes through a painful section on how the goodwill impairment charges could have been avoided if the business had been lumped under a bigger business. I think since the entity was not bought as part of a bigger company, the goodwill must be evaluated at the entity level balance sheet. When one pause and thinks about it, it does not put Markel’s management in very good light. It will very important to keep track of Markel Ventures as it becomes a bigger piece of Markel. More disclosure in Markel ventures would be a welcome change in the future.

Beyond that, the letter provided a good insight into the state of affairs at Markel. With Alterra being more conservatively reserved than before, the integration happening well, the insurance business performing robustly and the investment business roaring, Markel’s management no doubt deserves the trust of shareholders. The record that they have generated speaks volumes for the way the management runs the business. This is one no brainer compounding machine over the long run if bought at the right prices. At March 20th closing price of $778.5 and book value of 1.4, good performance is fairly baked in the price. It is no longer the bargain it was post the Alterra acquisition but definitely one worth holding in the books if one already has it.

Disclosure: Own shares of Markel.

Thomas Cook and Fairfax

Prem Watsa, Chairman and CEO of Fairfax Financials, has compounded book value at 21.2% and stock price at 19% since 1985. There was a great deal of excitement when Fairfax took over the Thomas Cook operations in India. All investors, value, momentum and traders piled up on the stock. The best analysis post the acquisition was provided by renowned value investor, Sanjay Bakshi on Thomas Cook as an investment vehicle for Fairfax in India. See here

Fast forward, a couple of years and below is what appeared on the annual report of Fairfax Financials in March.

It raises the following questions

- Looks like Thomas Cook will also be a acquisition vehicle but all big ticket items would go through this new entity.

- Given the fees that Fairfax would gain from the transactions through the new entity, it seems it is logical that the best of ideas might flow through the new entity.

- Why could Fairfax just not recapitalize Thomas Cook to be owned through an entity in Canada and issue more stock at the current price?

- Will there be any conflict of interest every time Fairfax uses the allocation vehicle instead of Thomas Cook to Thomas cook shareholders? Will Thomas Cook shareholders be shortchanged in the long run?

I have always been a big fan of Prem Watsa but it looks like the current move is more beneficial to Fairfax owners than to Thomas Cook.

Disclosure: Own shares of both Fairfax and Thomas Cook India

Biglari Holdings and Groveland Capital

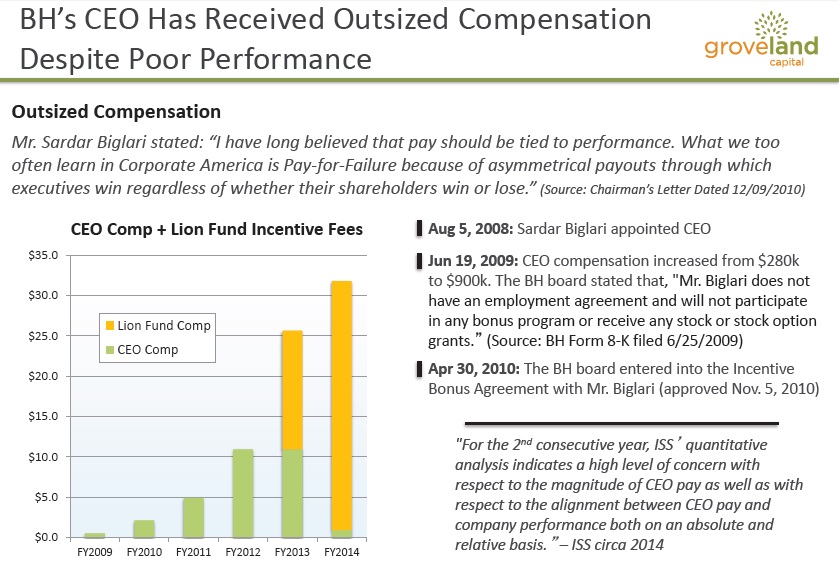

A very interesting fight seems to be brewing between two activist investors, the brash young CEO Sardar Biglari of Biglari Holdings and Groveland Capital. A tiny hedge fund with a 1% position in Biglari Holdings is trying to nominate its own board. Sardar Biglari, one not be backed down, published the following presentation in response to Groveland’s nominations and presentation here.

The main thrusts of Groveland objections are under performance against the S&P 500 and excessive CEO compensation.

From the first snapshot below, from a 1-year, 3-year and 5-year perspective, it does look like Biglari Holdings has under performed the S&P 500. In the long run, the stock price is the true indicator of value creation. Looks like Groveland does have some merit in their 5 year argument. We will look at Biglari Holdings 6 year test later.

The compensation for Biglari holdings has increased quite a bit with the Lion fund compensation that he has been getting over the last few years. So, it is indeed true that fees do look high with respect to the under performance versus the S&P 500. We will dive into the actual performance of the Lion Fund later.

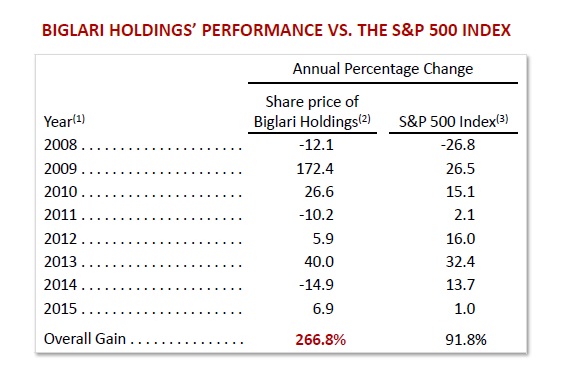

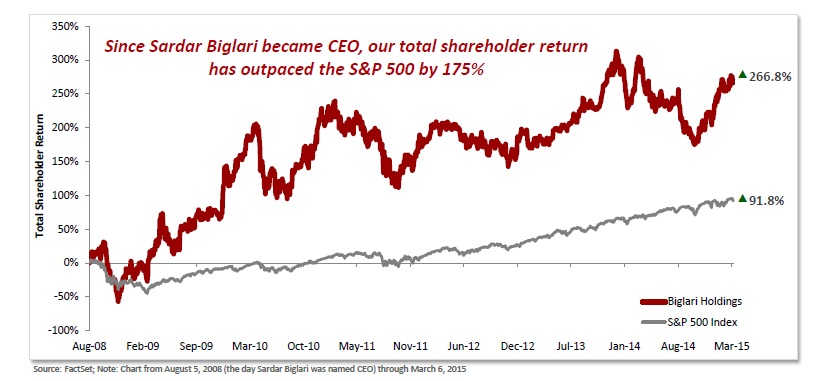

Biglari shot back with his own presentation in which he included the 2009 results to the mix. As all of us know, 2009 was when the markets started rising like a phoenix from the ashes. When we include the results of 2009, it paints a very different picture of the performance of Sardar Biglari against the S&P 500.

The question is it fair to include the 2009 results? Is 5 years a sufficient time frame to do reasonably well as against the market? Granted that Biglari Holdings had one great year in 2009 but since then the stock has not performed so well. When we look at the underlying business, there has been two rights offering as well where the shares have been diluted from a shareholder perspective.

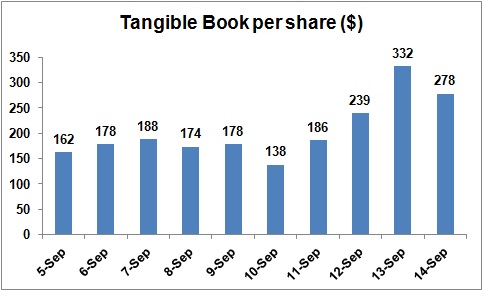

Given the disparate nature of the businesses owned by BH and dilution, perhaps growth in tangible book value per share is a better indication of the value creation at BH as against just the operating earnings. The one, two, three and five year CAGR’s are -16.3%, 7.9%, 14.2% and 9.3%. So, compared to the S&P 500 5 year CAGR of of 13.2%, it does look like the value creation has been sub par as against the market. It must be noted that even Warren Buffet has under performed during the last few years but on a company that is several hundred times bigger than BH.

To justify the performance fee that Sardar Biglari has been drawing through the Lion’s fund, BH put up the following performance to justify the performance. The below chart shows outperformance every year as compared to the S&P500 but it has not resulted in book value per share gain for share holders even with the investment portfolio marked to market in the balance sheet.

While it is not clear how groveland capital can add any more value to this situation, it is also pretty clear that BH has not been creating tangible book value per share growth in meaningful way for shareholders to consider investment over the market. With a ego-driven CEO, untimely rights offerings, over the top compensation, the cautious investor’s best position would be in the grand stands watching the fight rather than participate in what will be a colorful match of activist investors.